The Mortgage Rate Mirage: Are We Seriously Calling This "Relief"?

Alright, let’s talk mortgages, because apparently, someone in power thinks we’re all idiots. You see the headlines, right? "Rates are softening!" "Relief for homebuyers!" And I’m just sitting here, coffee going cold, wondering what alternate reality these folks are living in. Because from where I’m standing, it looks like the same old song and dance, just with a slightly different, equally depressing, tempo.

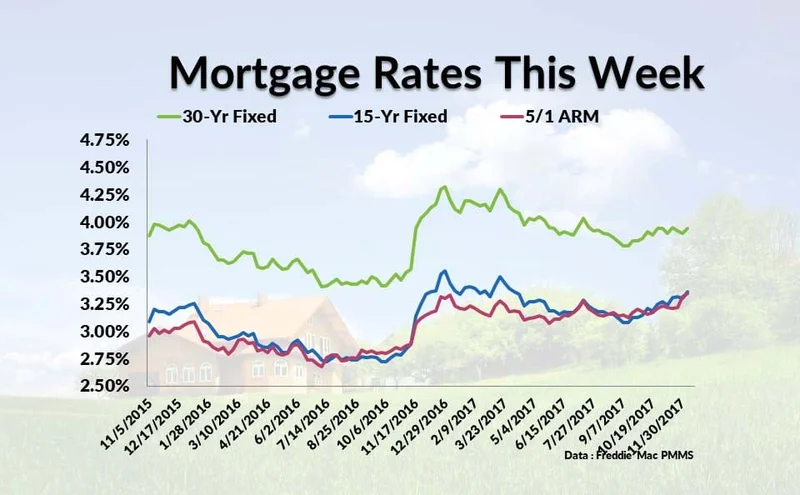

We got the Fed, bless their hearts, cutting the federal funds rate twice this year—once in September, once in October. The first cuts of 2025, mind you. And what happened? Did the heavens open? Did mortgage rates plummet? Nah, not really. We were all told to expect some big, sustained drop, like a dam breaking, but what we got was more like a leaky faucet. You look at the data from November 21st, 23rd, 24th... 30-year fixed conforming rates bouncing around 6.244%, then 6.11%, then 6.236%. A basis point up, a couple down. It’s like watching a really boring tennis match where no one ever scores. This ain't "relief," folks. This is them dangling a slightly smaller, still very expensive, carrot in front of a starving horse. And honestly, it’s insulting...

The "Golden Handcuffs" Are Real, And They're Tightening

I've talked to enough people, heard enough stories, to know what’s really going on. You’ve got millions of homeowners out there, stuck in what we’re now calling "golden handcuffs." They bought their places when rates were ridiculously low, like that sweet 2.65% back in January 2021. Now, they're trapped. They want to move, expand, downsize, whatever. But the thought of trading a 2.8% rate for anything north of 6%? Forget about it. They’re stuck, literally watching their lives stagnate because the housing market is playing this cruel game. I mean, imagine being a young couple, eyes glued to Zillow, seeing these daily rate shifts that barely register. That gnawing feeling in your stomach, the one that tells you you're still priced out, still waiting for a miracle that ain't coming. It’s a gut punch, day after day.

And what about those "expert" opinions? They’re quick to remind us that 7% isn't historically high, that rates were common in the 70s and 90s, even 18% in '81. Yeah, great, thanks for the history lesson. But we don't live in 1981. Wages haven't kept pace. The cost of everything else has exploded. My grandpa could buy a house on a single income. Try doing that today, even with rates at 6%. It's a completely different economic landscape, and comparing it to some bygone era is just plain ignorant. Or maybe, it’s just a convenient way to tell us to suck it up. I'm not sure which is worse. This is a bad situation. No, "bad" doesn't even begin to cover it—it's a systemic chokehold on an entire generation's financial future.

The Federal Reserve's Crystal Ball, Or Just Blind Luck?

Now, let's talk about the future, because that's where the real anxiety lies. We've got another Fed meeting slated for early December. Will they cut again? Who knows. It’s like trying to predict the weather based on a groundhog. And then you throw President Trump’s policies into the mix—tariffs, deportations, all that jazz. Some smart folks are already whispering about how that could constrict the labor market and, you guessed it, resurface inflation. Because that’s what we need, right? More inflation to drive rates even higher, just as we thought we might catch a break.

The Fed says they influence rates, but they don’t set them directly. They mess with the federal funds rate, they manage their balance sheet, shrinking holdings of mortgage-backed securities to push rates up. It’s all these levers and pulleys, this intricate dance, and meanwhile, regular people are just trying to figure out if they can afford a roof over their heads. Why is it always so complicated? Why can't we get some straight answers, some genuine stability? Maybe I'm the crazy one here for expecting a little less financial wizardry and a little more common sense. You gotta have excellent credit, a low debt-to-income ratio, and then you gotta shop around like your life depends on it, just to save a few hundred bucks a year. It's like they want us to jump through hoops made of fire, offcourse, just to get a slightly less terrible deal.